I’ll tell you this: I was never the sharpest knife in the drawer. Or the smartest kid in class. In fact, I suffered from a learning disability all throughout school because I didn’t pick things up as quickly as my classmates.

I had to work harder. Longer.

For me, getting an A in a class was an achievement, and I never took them for granted. I envied my classmates for what seemed like a magical ability to just get it. Almost instantly.

But, I was never able to do that. Why am I telling you this?

I’m telling you this to prove that you don’t need to be a genius or the best in your class to figure out money.

While money will come easier for some of us than for others, the concepts behind building wealth aren’t complicated. And, the money principles I used to achieve my goals are straightforward.

I retired at 35 from full-time work. Each and every day, I get to choose exactly what I do with my time. Like hiking and house projects. Blogging or, hell – just taking a nap in the afternoon, the freedom to control my time is a freedom unlike any other.

Building enough wealth to retire takes time, but like I said, the concepts are not difficult. Below, let’s take a look at the 5 money principles I used to retire super young, and how you can take more control over your finances and make your money work for you.

You won’t need to be a gifted student or a highly-paid professional to start putting these money principles into action right away.

They are accessible to anyone.

If you’re interested in a little more, don’t forget to check out my early retirement FAQ. Juicy details. 🙂

The 5 Money Principles I Used To Retire At 35

First, let’s get one thing straight: Not everyone will be able to retire at 35. I am not under the illusion that if we all would follow the exact path I did, that we would all be happily unemployed in our mid 30s.

That’s just not realistic. But, I do firmly believe that achieving financial freedom is within the grasp of a lot of us. More than we probably realize. It may not be easy. It might take sacrifice.

But, it’s there. It’s reachable. All you need to do is reach for it.

Money Principle #1: Make financial freedom your goal

The first principle has nothing to do with money. Money is the means in which to achieve financial freedom, but there’s something much more fundamental that needs to be addressed first.

Financial freedom isn’t something that just materializes.

It’s like getting into shape. Most of us won’t lose weight or gain strength by refusing to change our habits and prioritize fitness and diet. It won’t happen. Life doesn’t work that way.

Financial freedom – as with getting into shape, takes drive and dedication, and the first step is to make it our primary goal. What drives us. We need to want it.

Let me say that again: We Need To Want It.

Once we set our minds to achieving a goal, human beings tend to implicitly begin to make decisions in support of that goal. We might go out to eat less and cut back on monthly subscriptions (like cable television). We might even keep our cell phones longer than just a year before upgrading them.

We’ll ask our employer or bank to automatically save a portion of our paycheck into a retirement account for us.

In other words, it won’t be a mental struggle to save instead of spend when financial freedom is our #1 priority.

And, we won’t miss the money because we know where it’s going. It’s building up into something powerful. Something that’ll enable us to achieve the freedom and liberty to design our own lives.

…outside of full-time work.

Money Principle #2: Invest in appreciating assets

While it’s true that nobody ever got rich by spending money, let’s take this one step further.

Nobody gets rich just by saving money.

Nobody ever got rich just by saving it, either.

Saving money is better than spending it, but wealth is built by investing our money into appreciating assets. Examples include:

- Stock market

- Real estate (property or homes)

- Businesses

- Relics or historic objects

The idea behind this is simple: we buy an asset (for example, a share of stock or a piece of property) for a certain price. Over time, the asset appreciates (or increases) in value. And boom! Now we have something that’s worth more than what we paid for it.

But, here’s the magic:

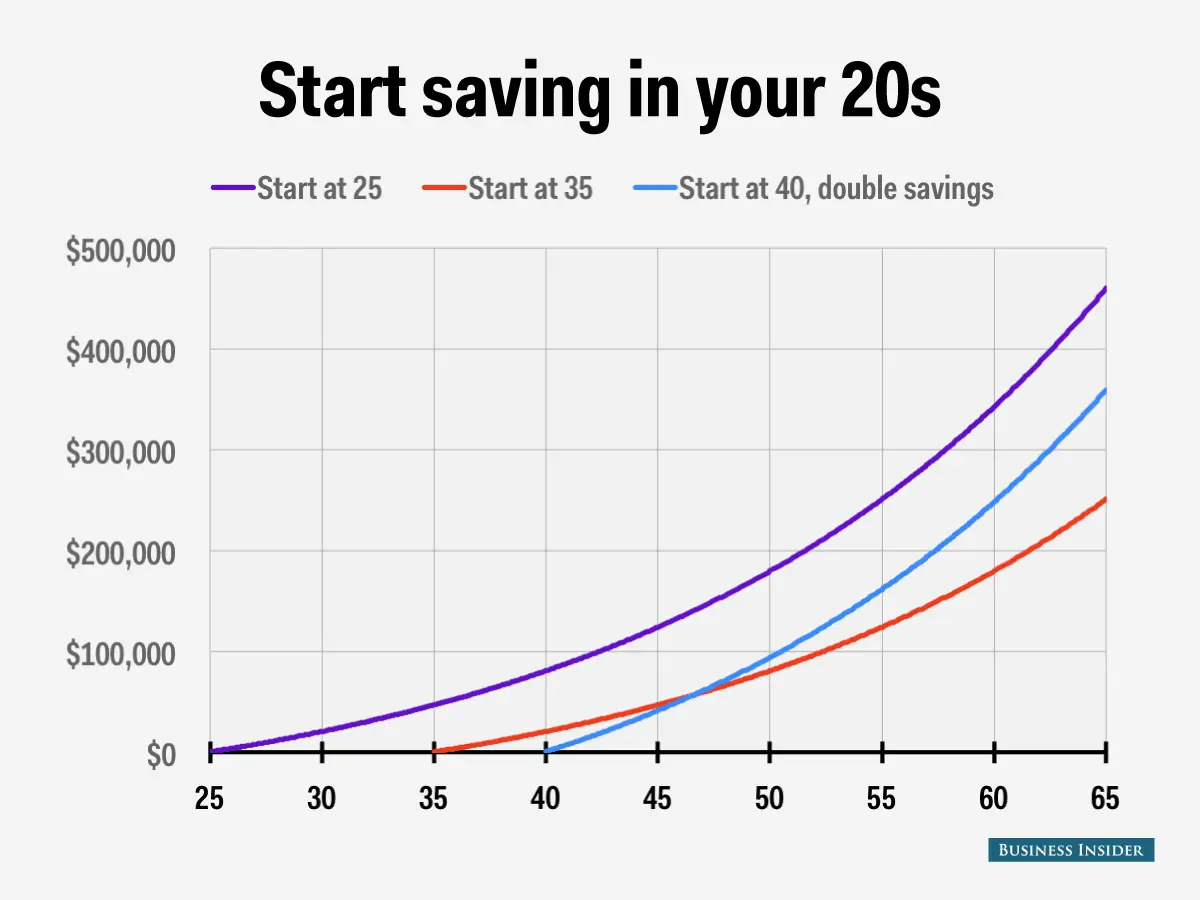

Through the power of compound interest, our assets don’t just build linearly. Instead, appreciating assets build exponentially.

It’s a curve, not a straight line.

Compound interest means your assets build upon themselves.

If you invest $1,000 and it appreciates 10% (or $100) in a year, then your new base starting point in year two is $1,100. Another 10% gain is $110, not just $100.

Add a couple of zeros to those numbers and we begin talking about quite a bit of money. Enough money on which to retire.

It’s almost like magic, except it’s not. It’s real, and it’s how I built up enough wealth to retire in my mid-30s. I started investing when I was young. In high school, actually. My dad made me do it.

And, I owe a lot of my success to my dad. His inspiration and teaching had a huge impact on my life, and it’s something that I’ll never forget.

But…

We all don’t have to start investing in high school to retire early.

Regardless of age, if you haven’t started investing in appreciating assets, start. Start by talking with your HR department at work to find out about your options. Or, speak with a trusted financial advisor.

When it comes to investing: late is better than never.

Money Principle #3: Automation

Here’s a clever trick to make sure you’re saving and investing every month: make it automatic.

Just like a machine.

Taking the discipline out of your savings plan will drastically increase your chances of success.

Many employers offer 401k or IRA retirement plans. And, most of those companies will automatically make contributions straight from your paycheck into your investment accounts.

Once it is set up, you’ll never have to worry about it again. It just happens, like clockwork. No discipline. No remembering.

When we put our finances on auto pilot, things just happen through the magic of automation. We used this to the fullest back when my wife and I worked full-time jobs.

- We automatically contributed to our 401k and IRAs

- We automatically transferred money from checking into savings

- We automatically paid our credit card bills so we *never* ran a balance

Automation helps to ensure those repeatable and dependable processes that need to happen every month…happen. We aren’t relying on our discipline to pay bills to avoid late fees and interest.

There’s a reason why we’ve never paid a single interest charge on our credit cards. Never a late fee. No reductions in our credit score (if you even care about that).

This is all due to setting up automated processes that guarantee that things happen when they need to happen.

Money Principle #4: Expert-level knowledge of cash flow

I have not met very many early retirees or people who are financially free who don’t have a precise understanding of exactly where their money is going. Virtually every dollar.

This is called cash flow.

Each month, money comes in and money goes out. For most of us, money comes in through our paychecks. It might also come from odd jobs we do for extra cash or by finding a crisp $20 on the street.

Money also goes out. Our rent or mortgage. Food. Restaurant spending. Cable television and our cell phone bill. Anything else we buy or spend money on during the month. That’s money out.

Together, a detailed understanding of your cash flow (money in vs. money out) means you know exactly what you’re spending money on and, ideally, how much money you have to spend.

This is one of the most basic money principles of all.

Remember:

- Look at your bills instead of throwing them aside; make sure you understand every line item on your bill

- Discretionary spending (“fun” spending) should come after paying your bills and funding your retirement accounts

- Monthly subscriptions are notoriously forgotten; be sure that you are aware of all of your subscriptions that cost money

- Small expenses add up fast; morning coffees, lunches out, grabbing a bag of beef jerky, etc…all add up

Remember, my advice isn’t to cut out all discretionary expenses tomorrow. Instead, my advice is to know exactly where your money is going. Only then can you make smart decisions about where to cut spending.

Money Principle #5: Eliminate your debt

Here’s something that you might not expect me to say: Debts aren’t always bad. It’s true. If used properly, debts can better position us to make money over the long haul.

For example, loans to build new businesses or improve our level of education can certainly benefit us beyond what we paid.

However, many of us aren’t taking on debt that way. Instead, most people use debt as a means to spend money we don’t have.

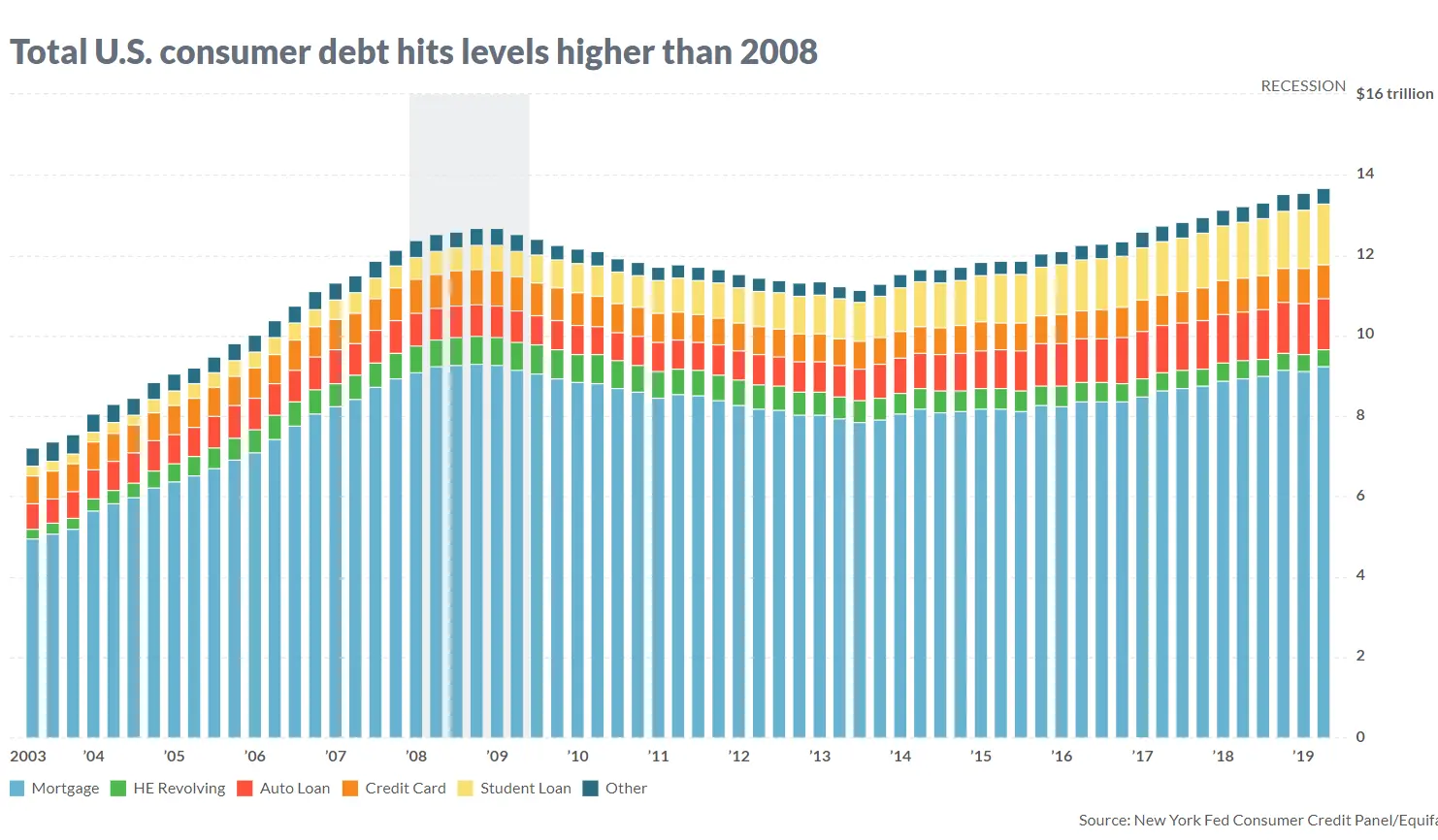

If you look at total consumer debt in the United States, it won’t take long before you realize that there’s a big, big problem here.

In fact, today’s debt is above what it was during the crash in 2008.

Too many of us are spending money that we don’t have, and we aren’t necessarily using debt to improve our lives. And when we are buried under mountains of debt, it’s almost impossible to build wealth because we are digging ourselves out of a hole.

And with a recession that’s bound to hit in the near future, debts prevent us from recession-proofing our finances.

Again – financial freedom doesn’t necessarily mean that you have NO debt. Life isn’t that simple, and neither is financial freedom.

Instead, it means that your debts haven’t put you into a position of weakness by spending money on things that depreciate in value and hurt your financial position.

When it comes to debt, those who are financially free:

- Establish and maintain a good financial position (ie: emergency fund, retirement savings, etc) before accepting debts – for the exception of student loans younger in life for marketable degrees

- Accept smart debts that are calculated and purposeful

- Never take on a debt that you cannot pay back

Use debt as a tool, not as a way to spend money that you don’t have. Smart debts are those that improve our future and support our longer-term goals. Smart debts are good debts.

Don’t accept any other kind.

How Many Money Principles Do You Use?

This is a judgement-free zone. I’m not here to criticize your money choices, and you shouldn’t beat yourself up if you’ve made mistakes with your money (I have too, believe me!).

By using these money principles, my wife and me set ourselves up to achieve financial independence and retire early at the ages of 34 and 35, respectively.

Financial freedom is a feeling unlike any other.

Are you ready to take that first step? If so, good! Start with the very first principle and make the decision to prioritize the goal.

Make it permanent. Then, make everything else automatic.